The Golden Years - Werking Your Retirement

I remember getting my job back when I was 15 at Hardee’s and completely passing out when I got my first check! Babyeee - those taxes and deductions made it hella hard to drop fries anymore that day. But, I did --- you know, to get paid. But one of the lines that stuck out to me was about Social Security. With talking with my Mom I got some more insight in what that was and how they played into my plans later on in life.

Then in High School, both of my parents gave me the juice about 401Ks at their place of employment. While the conversation didn’t grab my attention too much, it connected like Golden State during the first couple of days within my first “Corporate” job out of college. I was then met with not only S.S. deductions but my 401K deduction. The more you make, the more they take is somewhat true. But at the time, I didn’t ‘get’ the purpose of matching and stacking. My how things evolve don’t they.

But some people don’t see the importance of retirement planning due to the current pulse. Many people are seeing either their place of employment snatch back their match percentage or in the case of Exxon - halting contributions, period. Along with people seeing that they would better hold their stacks vs contributing to a fund that doesn’t feel fun at this moment. I get it, I expired that during the last recession when 60% of my 401K dipped hard. Heck, I held company stock and found it worth less than $5/per share. It was really Ghetto. Read more about that in this article.

Did you know that the average length of retirement is 30-40 years?!

It pains me that how to plan for retirement was not aligned for all, but for the affluent. Yet, you know how I feel about that. I wish more of not only the culture understood (and was shown), but 60% of society got it too. And even those who did save towards it, but finding out what they stacked isn’t a match for how much it takes to survive during times of inflation and changes in Social Security. Then you have other finance experts calling for society to have at least $1M+ in to withstand retirement, yet some might not even make that in their lifetime in plan. Heck, the pensions once loved have now lacked or non-existence. Plus, those with 401Ks, 403Bs don’t even grasp concepts such as asset allocation and how to read their portfolio within that fund. Target Dates are just a word, but not wrapped for them to understand it deeper.

Did you know that if you are feeling behind in saving for your retirement, you can look into 401(k) Catch-Up Contributions if you’re 50 or older. You are able to contribute an additional $1,000 (+) to the already set limit.

But back to the current stance with the romance with retirement; it is hard to see the long term gain when it comes to saving for later on in life when you could just place some money into a CD or any other account. I get it, but there is something that I want us to grasp when it comes to retirement. The same way that we are told to have multiple streams of income that doesn’t mean right now, that means later. That 401K, IRA, Annuity, Life Insurance, Self-Directed (Solo) 401K (for my entrepreneurs) or any other retirement wealth vehicle can be streams of income during the Golden Years as well. Social Security can only pay out a percentage, which isn’t close to the day-in and day-out expenses you might find yourself with later on.

Here are some things to keep in mind when planning for those years for you to relax and not stress:

Retirement Pulse: Do a check quarterly to see not only where you are saving for retirement, but the ways you are saving. Does your employer match? Are you inching towards that currently. If you can’t fully contribute, bump it up each quarter until you hit it. Don’t feel bad, feel out a strategy to get it.

Tap in with your expenses: Not only monthly and annually, but each decade to see how much it takes to survive. You can keep tabs on inflation, but for you to see how your eggs are stacking up to support you without worry during those years.

Do you have money elsewhere? People switch jobs like the weather switches up on us. If you have switched jobs in the past, did you contribute to a plan then? If so, roll that over into an IRA (Roth) where you can manage it better to save or even purchase passive income stock.

Take it up a notch. Can you move beyond the 401K/403B? Look into Annuities, IRAs or even Life Insurance policies to stash your retirement cash! In building wealth, we should always be looking for ways to diversify not only boards, but our bank (accounts).

Each year our friends over the IRS gives us updates on contribution limits when it comes to IRAs and 401Ks. For the year 2000 21, the limits are not changing to where they currently are. Keep in mind, this applies to 403Bs, 457s, TSPs (Thrift Savings Plan). That magic number is $19,500.

But, there was a change when it comes to Roth IRA income limits. If you are single single + your income is under $125,000 (the current income limit, up from $124K in years past), you can make contributions to your Roth up to $6,000 (+ $1,000 for those having to catch up). For those married, y'all income level has moved up to $198,000. To get some more tea on other retirement accounts, peep this from the IRS (click here).

Inside tea: You are only allowed to contribute to a Roth if your income is underneath a certain threshold. Also, look into “Backdoor Roths” in case you are outside of those income limits. There is always a way to do things. Mr. $750 taught us that.

So have a money meeting with your retirement accounts and strategy to see where you are and where you hope to be when you chuck the deuces to working (for someone else or period). Here are some additional resources:

Call up your retirement folks to get a pulse on how your Target Fund and those funds are looking. Your employer pays for you to call them up to keep in touch with your money. Also, learn more about allocating!

Look to see what other retirement funds you might have out there. From old employers, etc. Here’s what you can do with them! Watch this!

Grab my “Stack or Slack: The Quick + Derrty On Savings” or “The Start” guides. I give some tea on IRAs along with saving within it.

Snatch a session to walk through your strategy with you.

Create your financial objectives. Know what they look like. “Being rich” is good, but get more specific.

Also, here’s an amazing book to help you shape your thoughts into retirement planning!

The scale is in the start, Fam. No matter if you are catching up or starting up - just do it. Give yourself grace for making sure you touch as much green as possible! Lessons give us leverage to do even better than what we imagine.

Updated context for the content!

Since I pushed this original post so much has happened.

A lot of people have lost their jobs. Stop contributing to their 401K (pandemic or not, life happens). Or even shifted jobs. I’m going to have this become an evergreen document on Retirement Planning. Sure there will be separate articles, but this will be the nucleus.

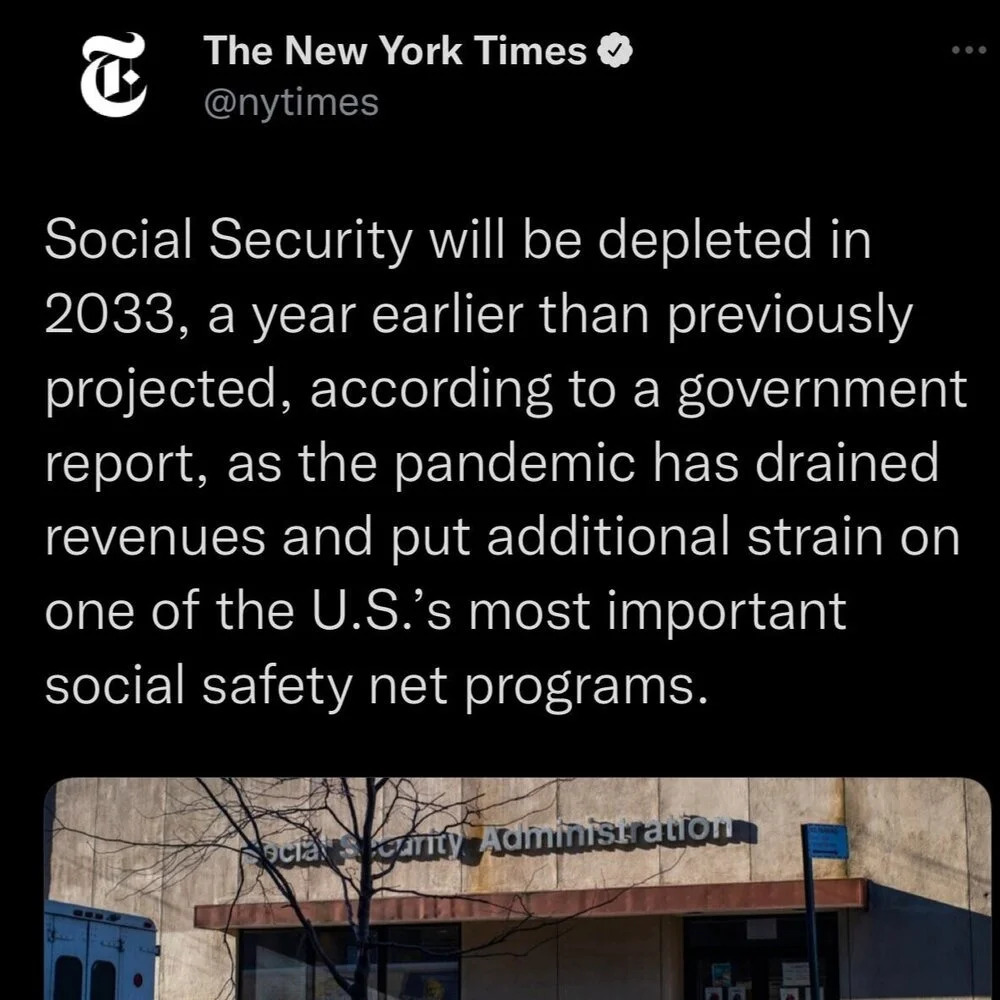

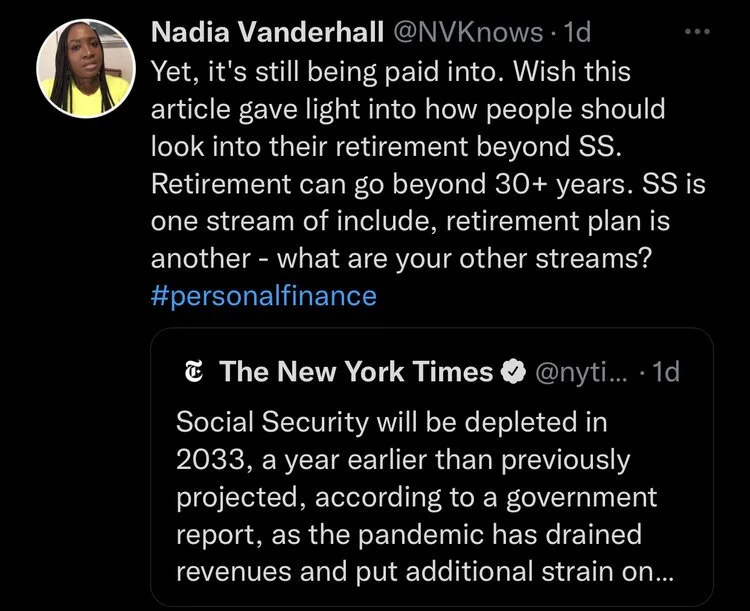

Also, since we left off - news came out that due to the pandemic and the shift in the workforce (people not working or things happening) that it is projected that Social Security will run out sooner than expected. 2033. Yall. Click here to read the article for more insight.

While this isn’t shocking, what I questioned via Twitter is that we are still paying interest into this depleting bank account. But gave some context into how we can start taking our own golden years into our own hands. Pensions are gone. Social Security is lackluster. Some companies are phasing out matching. What are you doing to start funding those golden years?

Again, start really thinking about how you want your retirement to look and feel. What lifestyle do you want to live? How much does that lifestyle cost and how does inflation counter that price tag. There are retirement calculators (Google or use this one) that can help you add it up!

Some more references that I want to call out -

Retirement Ready:

Worksheets from Social Security (Yes, that one) that can get you on par with retirement. I rarely see these floating around. They are by ages 18-48. 49-60. 61-69+.

Check out my book list as I update to see what books can help you along your journey!

As I learn about more information and insight, I will share! Wealth is a journey, retirement is just another layer to look towards. Also, you can create income streams at any point in life. Never too late to start!

Reference Reading:

Legacy, Legacy, Legacy....Planning With Life Insurance

Don’t Stop.. Get It, Get It.. Saving With High Yield Saving Accounts

Financially Speaking. Formulating Your Financial Objectives.