How To Bounce Back: Rebuilding Your Retirement After Hardship Withdrawals

Life happens. Unexpected expenses like medical bills or home repairs might lead you to dip into your retirement accounts for quick cash. About 25% of workers have taken hardship withdrawals from their 401(k)s due to job loss and rising costs. I even remember this article about how retirement funds have become the new ATM. While this can provide immediate relief, it’s vital to have a game plan to rebuild your retirement fund afterward.

Understanding Hardship Withdrawals And Loans

So, what are hardship withdrawals? These are typically used for urgent needs like medical emergencies, evictions, or funeral expenses. Some employers even offer loans against your 401(k) that you'll need to repay with interest. Be cautious, though—if you're under 59½, you could face taxes and a 10% penalty on withdrawals. The SECURE 2.0 Act has made it easier to take out emergency withdrawals, but you’ll still need to consider the tax implications.

Before making a withdrawal, review your HR policy to understand where you stand regarding hardship withdrawals. Additionally, inquire about other hardship programs your employer may offer.

Types Of Hardship Withdrawals

When you need to take money out of your retirement fund, it’s usually in one of two forms:

Hardship Withdrawals:

These are for specific “hardships” like medical emergencies, preventing eviction or foreclosure, college tuition, or funeral expenses. While this money can help during a tough time, it’s important to know that withdrawals are permanent—you can’t pay it back. Plus, you’ll likely have to pay taxes and penalties (usually 10%) on the amount withdrawn if you're under 59 ½.401(k) Loans:

A 401(k) loan allows you to borrow from your retirement savings to pay it back over time. The good news? You avoid the early withdrawal penalty. The catch is that if you leave your job, you might have to pay the loan back in full pretty quickly—or it gets treated as a withdrawal, which means taxes and penalties could kick in.

*Yes, you can get a loan/withdrawal on your 401K to buy a home but we are focusing on this scenario at the moment.

[If you have been laid off, read this]

Been There, Done That - A hardship withdrawal.

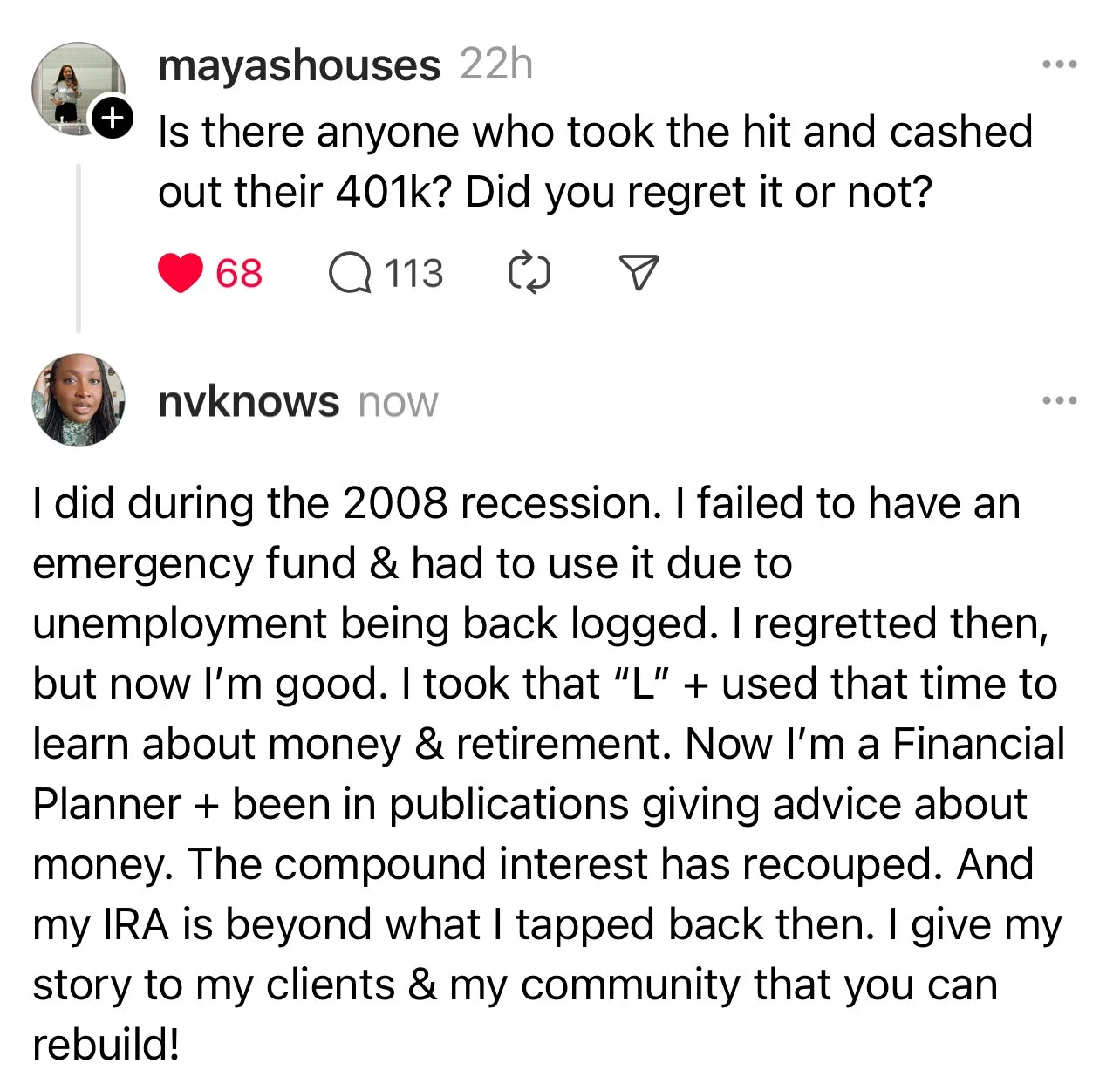

I know firsthand how tough it can be. During the 2008 recession, I had to cash out my retirement savings because I didn’t have an emergency fund (here’s tips on how to build after you break your fund). This was my first 401K out of school and to be honest - I didn’t know what I was doing. It was a hard lesson, but I used that experience to grow and become a financial planner. My retirement stack is back on track and I have multiple ones. Sharing my story to clients helps them see that setbacks can lead to better financial habits. So when I talked about my antics (of the past and present) on content and my newsletter, it comes from a place of showing you that I get it. That same feeling is seen when I work with my clients as well.

Understanding Hardship Withdrawals and Loans

So, what are hardship withdrawals? These are typically used for urgent needs like medical emergencies, evictions, or funeral expenses. Some employers even offer loans against your 401(k) that you'll need to repay with interest. Be cautious, though—if you're under 59½, you could face taxes and a 10% penalty on withdrawals. The SECURE 2.0 Act has made it easier to take out emergency withdrawals, but you’ll still need to consider the tax implications.

Things To Consider Before Withdrawing

Taxes and Penalties: Understand that taxes and penalties can take a big bite out of your withdrawal. Calculate these costs before deciding.

Timeline To Payback: Outside of interest that could be applied to your withdrawal, be mindful that some servicers will only allow 1 per year or 1 loan/hardship until you pay it back. Budget for your having to pay it back. Make a plan for your paper ( money).

Replenishing Funds: If possible, aim to replenish the money taken out of your account within three years. This helps minimize the impact on your long-term savings.

Employer Rules Vary: Not all hardship withdrawals or loans are created equal—some employers offer more flexibility than others. According to a recent report, about 50% of companies allow 401(k) loans, but hardship withdrawal options can vary based on the employer. Make sure to check with your HR department or retirement plan provider to understand your specific plan's rules.

Rebuilding Your Retirement Fund: Give Yourself Grace

First off, be kind to yourself. Withdrawing from your retirement is sometimes unavoidable. Here are strategies to help you get back on track:

Gradually Increase Contributions: Once stable, aim to increase retirement contributions. Even adding 1% of your income can make a difference.

Consider Repurchasing Withdrawn Funds: Check with your employer about the possibility of repurchasing withdrawn funds to recover lost ground.

Set Up An Emergency Fund: Build an emergency fund of 3-6 months of living expenses in a high-yield savings account. Start by saving one month’s worth to understand your financial formula while gradually reaching your core goal.

Other Retirement Stack Tips

Restart Contributions ASAP: Contribute to your retirement fund as soon as you can. If your employer offers a match, contribute enough to maximize that benefit.

Reallocate and Repurchase Later: If you sold investments at a low point, don't worry. Reallocate when the market improves and continue contributing regularly.

Take Advantage Of Catch-Up Contributions: If you’re over 50, utilize the IRS's catch-up contributions—an additional $7,500 for 2024—to recover faster.

Automate And Increase Over Time: Automate your contributions and aim to increase them by 1-2% each year for a significant long-term impact.

Conclusion

I get it—I've been there before. Life can throw unexpected challenges your way, leading to tough financial decisions. This article is meant to empower you and enlighten you on your options, showing how a setback can become a step up toward your financial goals. Remember, your "Ls" give you leverage. With a solid plan in place to rebuild your retirement fund, you can navigate these hurdles effectively. By understanding your options and making gradual improvements, you can regain control of your financial future.

Stay Funded, Friends.