Difference: APR x APY

There are so many acronyms when it comes to money, you don’t know whether you are reciting the alphabet or spelling out words in the ground (10 points if you know my reference). The whole world of money can be one that is confusing and can completely turn folks off from learning about it. This platform is working to recorrect that stigma.

When it comes to The Culture, some foundation pillars for us closing the wealth gap is awareness and access. While they both start with the letter “A”, they are often the key points from people doing better with their finances. Yes, building a stellar budget and spending habits are key; yet when it comes to knowing what to do with the bands after that is where a lot of us fall short. I get it and never judge people for starting their budget for the 50-11th time. Why? It takes the right step to get in formation with your goals.

As I scroll through social media, I often see people talk about two things - their credit and credit cards. Both are important factors when it comes to another “C”, not Crip, but cash! How? Your credit score is key to how much you pay for loans or even your home/renter/auto insurance. It is also critical for being approved for other services like your electricity. Where am I going with this? Hang tight, Fam.

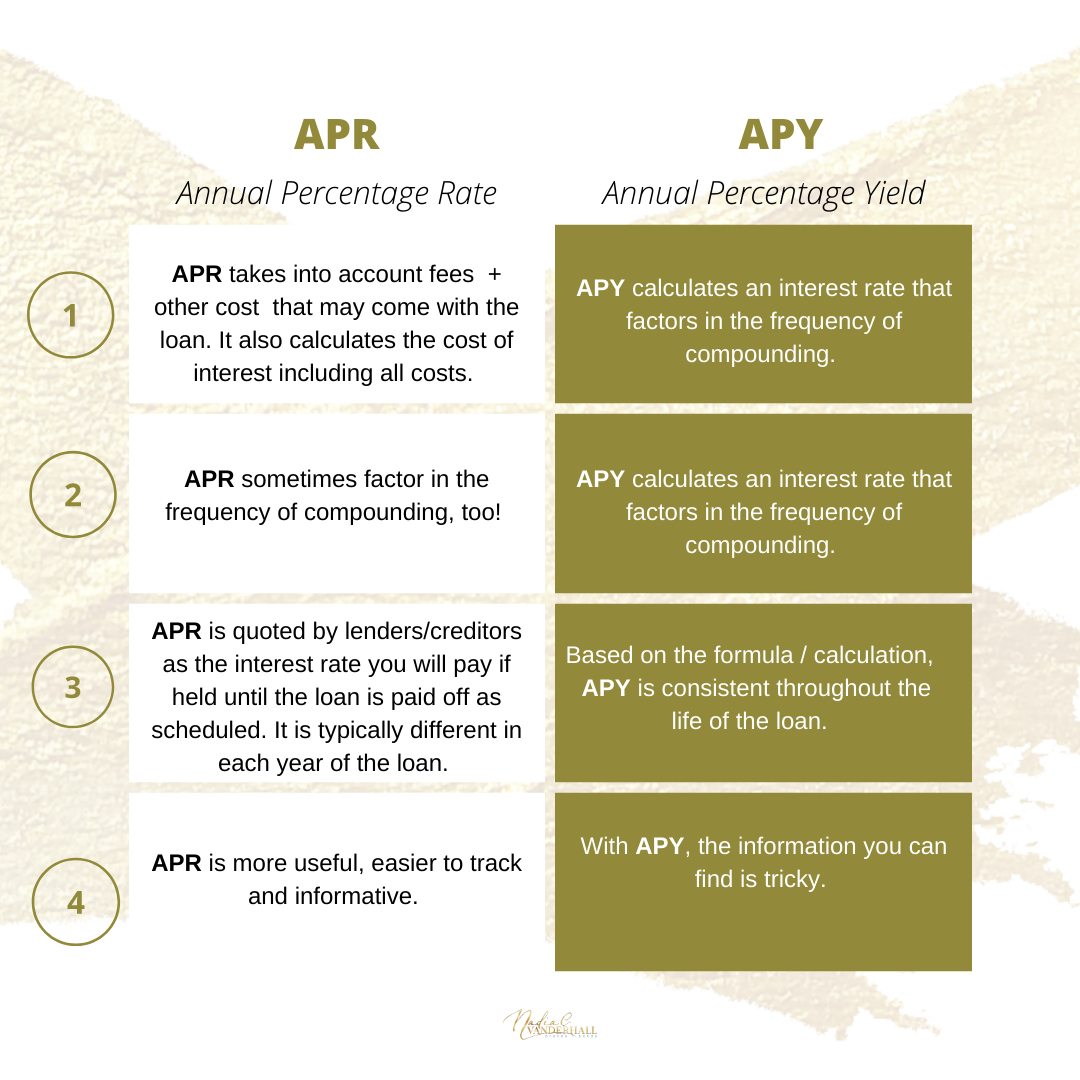

With your credit cards and stacking cash, two acronyms are major but often confused! APR x APY! APY and APR are both standardized measures of interest rates expressed as an annualized percentage rate. The first two letters are the same, but that last one means totally different for each type of account:

From the cart above, you get the vibes for what each means for certain accounts. If you haven’t caught the wave, let’s take it a bit deeper -

For anything loan based, your interest is calculated through APR or Annual Percentage Rate is used to determined the cost that you owe for utilizing their funds. This type of interest rate is used typically by you obtaining mortgages and auto loans to credit cards. Within using your credit card, APR is used to help you compare how expensive a transaction will be on each one. Be mindful. Most credit card companies gives you a bit of grace when swiping. Typically APR hits for credit cards - Purchase, Cash, Penalty + Introductory APR.

When it comes to your mortgages and auto loans - peep to learn how your creditor applies that to your loan. Also, look to see how much of said payment is going to the principle and the interest. Don’t become annoyed by it, plan it. If both of these types of loans have recurring interest that is keeping you paying for that house, car or credit card longer - look into refinancing or moving that loan to a Credit Union.

Now over to APY or Annual Percentage Yield! This is done mostly when it comes to accounts like High Yield Savings (bae), CD or traditional savings. APY is the actual rate of return that will be earned in one year if the interest is compounded. Compound Interest is your key when it comes to playing long-ball with your wealth building! Compound Interest is added periodically to the total invested, increasing the balance. The more you save and the more it compounds - the better!

So, here’s how both are calculated:

I outlined this even more in my eGuide, “Stack or Slack: The Quick + Derrty On Savings” (grab your copy here). Learning the difference will show you how you are saving within accounts that pay you and on the other hand saving on interest rates for accounts you pay. Difference.