Conquering Tax Season: Resources, Tips, and 2024 Tax Changes

Is it me or does it seem like every year tax season becomes even more taxing than the next? This year appears to not be any different. I’ve been getting inboxes and such about how people are having to shell out more bucks this year. The commentary about how the tax system works can be draining, but what drains people is the lack of resources and how to use them to help your wallet. As part of your financial planning, understanding and leveraging what you can within your tax planning is key - no matter the income.

In this blog post, I want to not only give you free resources that I’ve shared on CapWay but also some things to keep in mind before April 15, 2024! Yet, some of these things could help you set up a system for the next tax season by what we chat about in this post. While I can tell you that you must file early, I want you to feel empowered to do the pre-work when it comes to tax planning no matter the budget.

I’m noticing the big commentary has been around the tax credits. What these are — they help reduce the tax you owe dollar for dollar. Let’s get into this extensive post —

Part 1: Resources for Filing Taxes:

Free/Low Spend Options:

Who doesn’t love free? While I love quality for a low quantity, I wanted to start by giving you places to look to get your books filed for the low.

You could qualify for either the Volunteer Income Tax Assistance (VITA) or Tax Counseling for the Elderly (TCE) programs based on certain qualifications. The TEC program offers free help for those 60 years of age and older, specializing in questions about pensions and retirement-related issues unique to seniors. Additionally, the IRS does a quality review check for every return prepared at a VITA/TCE site before filing. To find out more about them, check here.

Another resource for those over 50, is AARP! Their Foundation Tax-Aide isn’t talked about as much as it should be! While the AARP is for those within that age range, the AARP offers free help to any taxpayer. Their core focus is to assist people who are 50 or older and have low to moderate incomes.

IRS Free File: Guided preparation is another IRS-based option to help tax filers with an Adjusted Gross Income (AGI) of $79,000 or less. You get to ask simple questions, and they will do the math for you. Another perk with this resource is that even some state preparation and filing are free! If you qualify for a free federal return via Free File but are left hanging on a free state return, note that some states may also offer their free filing programs.

Did you know that some states, libraries, and organizations offer free or low-spend tax preparation? Google this to find them: “Free or Low-Cost Tax Preparation in (list your city and state) in 2024”.

Low-Income Tax Clinics (LITCs) are another filing resource, but the thing I will call out is to check to see what types of filings they will provide. Most focus on federal filings more than state filings. They are also run by universities with tax law programs or law students.

The MilTax Program is for those who are currently in the military or have a spouse or dependent child of someone who is in the military or has served in the military. Here’s more info about it.

FreeTaxUSA: Federal filing is free, but state filings are $14.99 per state.

Either/Or Options (Platforms):

TaxAct provides affordable digital preparation for individuals, business owners, and tax professionals. With TaxAct Free, it allows you to file your federal return for free and your state return for $34.95 per state! This service also has a ton of benefits to check out - from free prior-year import to FAFSA assistance. Their most popular filing level is the Deluxe which is $24.95. You can also get cash back from Rakuten if you use this service!

H&R Block Free Online: The “Block” offers a free federal filing option for taxpayers with very simple returns. However, you'll need to pay to file your state return or if your return includes certain deductions or credits. Prices start at $36.99 for their Online Deluxe state edition.

TurboTax Free Edition: TurboTax offers a free federal filing option for taxpayers with very simple returns. Similar to H&R Block, you'll need to pay to file your state return or if your return includes certain deductions or credits. Prices start at $39.99 for their Deluxe Online state edition.

Paid Options (People):

If you have it within your budget to spend to make sure that your tax filing is completed, here are some people that I’ve known people to use in the past or I can vouch for their services:

Kimberly Davis and team over at Financial Elevation - it's a full-service Accounting and Tax Firm and one of my biggest supporters!

Part II: Some things to consider:

Think about not only if you want to use free or paid, but also what is involved with your tax filing. If it’s complicated, get some help. Don’t try to shake your stack by yourself unless you’re getting hand-holding. What level of help could look like is based upon how your filing stacks up - write-offs, laws, credits. If it gets busy, get the help. I don’t want you getting fined or worse. I have a feeling the audits might be heavier this year. Consider the complexity of your return, comfort level, and budget.

What changed this year?

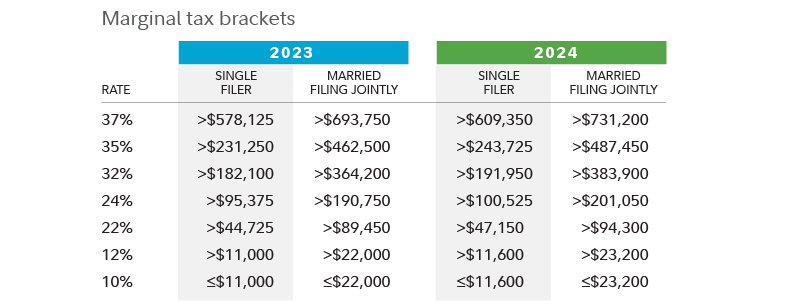

The brackets - no, not March Madness, but income tax. While there are still seven, how they shifted is interesting. The income ranges (tax brackets) for each rate have shifted slightly to account for inflation. For 2023, the following rates and income ranges apply.

The standard deduction increased. 2023 standard deduction increases to $13,850 for single filers and married couples filing separately and to $20,800 for single heads of household, who are generally unmarried with one or more dependents. For married couples filing jointly, the standard deduction rises to $27,700. Which is having some people in a tax tussle.

Itemized deductions are staying the same for the most part. If you have enough tax-deductible expenses, you might benefit from itemizing.

Retirement contributions boosted. Traditional IRA and Roth contribution limits in 2023 increased; Individuals can contribute up to $6,500 to an IRA, and those age 50 and older also qualify to make an additional $1,000 catch-up contribution.’23 contribution limits for tax-deferred 401(k)s and Roth 401(k)s have increased to $22,500. If you're age 50 or older, you qualify to make an additional $7,500 catch-up contribution for this tax year as well.

HSA also can get more stacked. While these health savings accounts have had people on their Zoom, this year the maximum you can contribute to an HSA is $3,850 for an individual (up $50 from 2021) and $7,750 for a family (up $100). People 55 and older can contribute an extra $1,000 catch-up contribution. Don’t have one, check out Fidelity and Bank of America. I talked about other financial apps here.

Child Tax Credit has been interesting to add up. This year, the Child Tax Credit is $2,000 per child under age 17. The credit is also subject to a phase-out starting at $400,000 for joint filers and $200,000 for single filers. For other qualified dependents, you could claim a $500 credit.

Alternative Minimum Tax (AMT) exemption is higher this year. These are like backup tax plans for high earners, triggered by certain deductions. The Tax Cuts and Jobs Act expires in 2025, and AMT will continue to affect mostly households with incomes over $500,000.

For those who have 529s and Estates (and other gifting-focused plans), this one's for you. The estate and gift tax exemption, which is indexed to inflation, rose to $12,920,000 for 2023. But the now-higher exemption is set to expire at the end of 2025, meaning it could be essentially cut in half at that time if Congress doesn't act.

One of the most common mistakes with tax filing is incorrect information. From your social security to accurate reporting of income and deductions to avoid potential penalties.

Yet, here are some ways to maximize your refund:

Earned Income Tax Credit (EITC): This refundable credit is specifically designed for low- and moderate-income workers. It can significantly boost your refund in many cases, even if you owe no taxes.

Child Tax Credit (CTC): Got kids?, claim the CTC, which offers a credit per qualifying child.

Other Tax Credits: Explore credits like the American Opportunity Tax Credit for education expenses or the Saver's Credit for retirement contributions.

Here’s a quick checklist of what you would need to get the full impact of your return. If you’ve already filed, use this checklist to get aligned better for next tax season:

1. Gather your Personal Info:

Social Security numbers and dates of birth for you, your spouse, and dependents

Copies of last year's tax return or any changes to them

Bank account number and routing number (for refund/payment); double check the banking info

Estimated tax payments: date and amount

Prior-year refund applied/paid with extension

2. Gather all forms of income:

W-2 forms: for you and your spouse (all employers)

Tips received: not reported on W-2 forms

With W2 Income you can still take advantage of:

401ks

HSAs

IRAs

529s

DAFs

CRTs

Roth IRAs

Real Estate

Tax loss harvesting

Maxing credits/deductions

1099 forms:

1099-NEC/K: self-employment income

1099-C / 1099-A Cancellation of debt information

1099-G: unemployment, state/local tax refunds

1099-INT/DIV/B: interest, dividends, other investments (Brokeages, Crypto, Retirement)

1099-R: IRA/401(k)/pension distributions

1099-S: sale of property

There are other 1099s based on your specific income sources (interest paid from savings, referrals of value over $600, etc)

SSA-1099: Social Security benefits

3. Other Forms of Income:

Miscellaneous income: stock options, gambling winnings, scholarships, prizes, etc.

Alimony received: Pre-2019 divorce settlements

4. Business and Rental Income:

(This is for business owners or real estate investors)

Rental property income/expenses: profit/loss statement, suspended loss info

Business income/expenses: profit/loss statements, expense records

K-1 forms: income from partnerships, LLCs, trusts, etc.

5. Gather Information for Relevant Tax Credits:

Childcare costs: provider info, tax ID, amount paid

Education costs: Form 1098-T; books, school supplies, other qualified expenses

Adoption costs: Child's SSN, legal, medical, and transportation records

Clean vehicle purchase information

Clean energy purchase information: solar, wind, heat pumps, battery storage, etc.

Health insurance purchased through the ACA marketplace (Form 1095-A)

For those auto gig workers, make sure that you get your mileage, car maintenance, gas, etc.

If you commute to work, don’t forget to add how many miles and how much you put in your gas to commute.

6. Itemized Deductions:

Mortgage interest: amounts on 1098 forms, escrow closing statement

Investment interest expenses

Charitable donations: cash amounts, receipts, property value, mileage driven

Medical/dental expenses (in excess of 7.5% of AGI): premiums, supplies, travel costs

Casualty/theft losses (federal natural disaster): damage amount, insurance reimbursements

State/local taxes paid: property, sales, income, vehicle license fees

7. Adjustments To Income:

Alimony paid (pre-2019 divorce settlements)

Student loan interest paid (Form 1098-E)

Teacher classroom expenses - IRA/retirement contributions (5498 forms)

Self-employed pension contributions

Health Savings Account (HSA) contributions

Self-employed health insurance payments

Moving expenses (military/state specific)

Ask your preparer if there’s any other information that you would need to make sure you get the most out of your filing.

Part II: Closing It Out:

If you find yourself having to pay dem people - please, please, please follow up on it. As someone who had to set up payments for the great state of NC, do it. Even if you don’t have enough to cover the full bill, you can always set up payments or look into other options to ease your load. If you feel you can’t pay those people and the bill is too high, consider seeing if an “Offer In Compromise” might work for your situation. Also, be mindful of any fees to set up payments, when the payment dates are, etc.

If you want to know what to do in case you do get a refund back, check out this other blog post. Heck, if you’re noticing that you’ve had to pay back the last couple of years - set up a savings account that will act as a sinking fund to help you get ahead of this annual bill. Please always check to see what you can write off ahead of time and keep your receipts. While some people see tax refunds as loans to the government, I see adding insight like this as telling people about the terms and conditions while knowing how to maximize the “loan” no matter your financial footprint. Use this season to be a way of tax planning for next.

Have you had a headache with taxes this year? What’s been the biggest ‘ugh’ for you?

Dassit.