Unestablished Wealth: Estate Planning

From the news to your newsfeed, over the last couple of years we’ve seen cases where Estate Planning was the topic. No matter if it was that it went well or went to hell, the fact of it all was that we’ve seen examples of both ends of the spectrum when it comes to making sure that the Estate had a solid foundation. Though we’ve seen GoFundMe campaigns, we’ve also seen social media content that gives lacks of context in the same regard.

While I’m not an Estate Planning Attorney, I’m someone (and a Financial Planner) who’s analyzed cases and learned about them through my previous employer as life experience. So while I give my insights, make sure you do your due diligence as with any insights that I prove. The reason why I am so set on doing this is due to the fact that within the African American Community specifically - we find ourselves dealing with Estate cases the most. No matter if we’re considered ‘common’ or celeb. Granted, it happens no matter the hue of skin, I know what I know. We’ve seen cases like Aretha Franklin, James Brown, Chadwick Boseman, and Prince among others to give tips on it happening - even someone closer. I know I have. No matter how ‘sure’ you think things are, there are more things that we could do to better maintain your Estate.

Oftentimes, we hear about getting a “Will” and some “Life Insurance”; which is true and I’ve spoken about Life Insurance types in another article. But I want to move into more focused territory. No matter if you feel that you have enough to consider your money and material things to be an Estate in your mind - it is. While I can’t give the full volume of what it takes to plan your Estate, I do hope that the tips, platforms, and updates of this post give you insight into what it takes for you to start yours.

When I saw Molly walk through her Mother’s Estate on Insecure and the commentary on Twitter about it, I knew that more of us needed to talk about it more freely and even get hip to what Probate could look like for us. I really appreciate that season for giving us more conversations that we needed to have as a community. But let’s get into what Probate is.

WTFinance is Probate?

Probate is a legal process that validates your will and settles your Estate. A court reviews your Estate documentation to ensure that the right people receive the right things; the clearer and more legally precise your will, the smoother that process will be. If a will is unclear, contested or found to be improperly executed, any fees associated with the lengthened court process are deducted from the Estate. A high probate fee could take roughly 10% of an average Estate.

Don’t worry if you feel that your Estate doesn’t look as massive as you want currently, we’re building as we go. Let’s talk through some tips I have, documents I suggests along with platforms I think you should research to get started with your process.

Now, some tips:

Make sure that you take an audit of all accounts (banking, retirement/brokerage accounts, life insurance, etc) and beneficiaries. If those accounts don’t have any beneficiaries listed - make sure they are ASAP. Make sure that your Estate Plan reflects this as well. Titles, deeds, etc need to be known. This will help with not only your planning, but also for the designated 1-2 people you will have over your Estate.

Know your Estate/Probate plan for the state you are in; if you move - lean into them.

Do a backtrack to see if you have any old policies that you need to claim.

Estate Planning doesn’t only mean you’re passing, disability is included as well. Group disability only covers 60% of your Net income and is partially taxable. Long term care is something to think about as well.

Also document your phone/Apple ID, bank ID account logins and passwords!

For your bank accounts: having someone listed as a beneficiary; it keeps the funds for going into probate. The beneficiary need only go to the bank with your death certificate and an ID of their own.

The beneficiary need only go to the bank with your death certificate and an ID of their own.

Note your state tax laws and how it plays into your Estate/Probate. You more than likely might get hit on the Federal level with some tax fees.

Review your Estate Plan at least annually. Life changes - you might have a child, make more or get a married - make sure it’s as updated as often as possible.

Documentations (some that I recommend; you can add more to customize your overall Estate Plan):

TOD/Transfer On Death: Deed if you own a home. Completing this document and filing it with your county saves your heirs money. It allows you to transfer ownership of your home to your designee. All they need to do is take their ID and your death certificate to the county building and the deed is signed over. Doing this will avoid the home having to go through probate. I would also add to make sure that they are listed on the deed prior as well.

Payable On Death (POD): These are agreements in which you have with your financial institution. Remember me stating to list your beneficiaries? This is why. This keeps your accounts from getting frozen like Elisa. It applies to all accounts at the said bank in question along with CDs. A POD arrangement is also known as a Totten trust. PODs are simpler to create and maintain than Trusts and Wills, but you should have it as part of your Estate Plan.

Living Will: This popular document allows you to put in writing exactly what you want done in the event you cannot speak for yourself when it comes to healthcare decisions as well as other final decisions.

Durable Power of Attorney: Allows one to designate a person to make legal decisions if one is no longer competent to do so. Keep in mind that this goes away when the person transitions.

A “Springing POA” combines Durable with ‘Non-Durable”.

Power of Attorney for Healthcare: This allows one to designate someone to make healthcare decisions for their person. There are other types of POA or Power of Attorney that you utilize within your Estate Planning (i.e. Medical, Traditional, Financial) . Again, these lapse when a person transitions.

Last Will /Testament AND Trust: Designates to whom personal belongings will go too. The latter keeps things in place. Trusts are also good if you have minors and they have to be the care of another adult.

Funeral Planning Declaration: Gives instruction to say exactly one’s wishes as far as disposition of the body and the services.

Life Insurance Policies: Yes, more than one. When you leave that employer the policy stays. But you have designated what you do with each policy. While there are 4 types, find the one that works for you - term works just as well.

HIPPA Release form type form.

This quiz from Trust + Will is quick and walks you through you thinking about what you might need. And this document from FreeWill is printable.

Platforms:

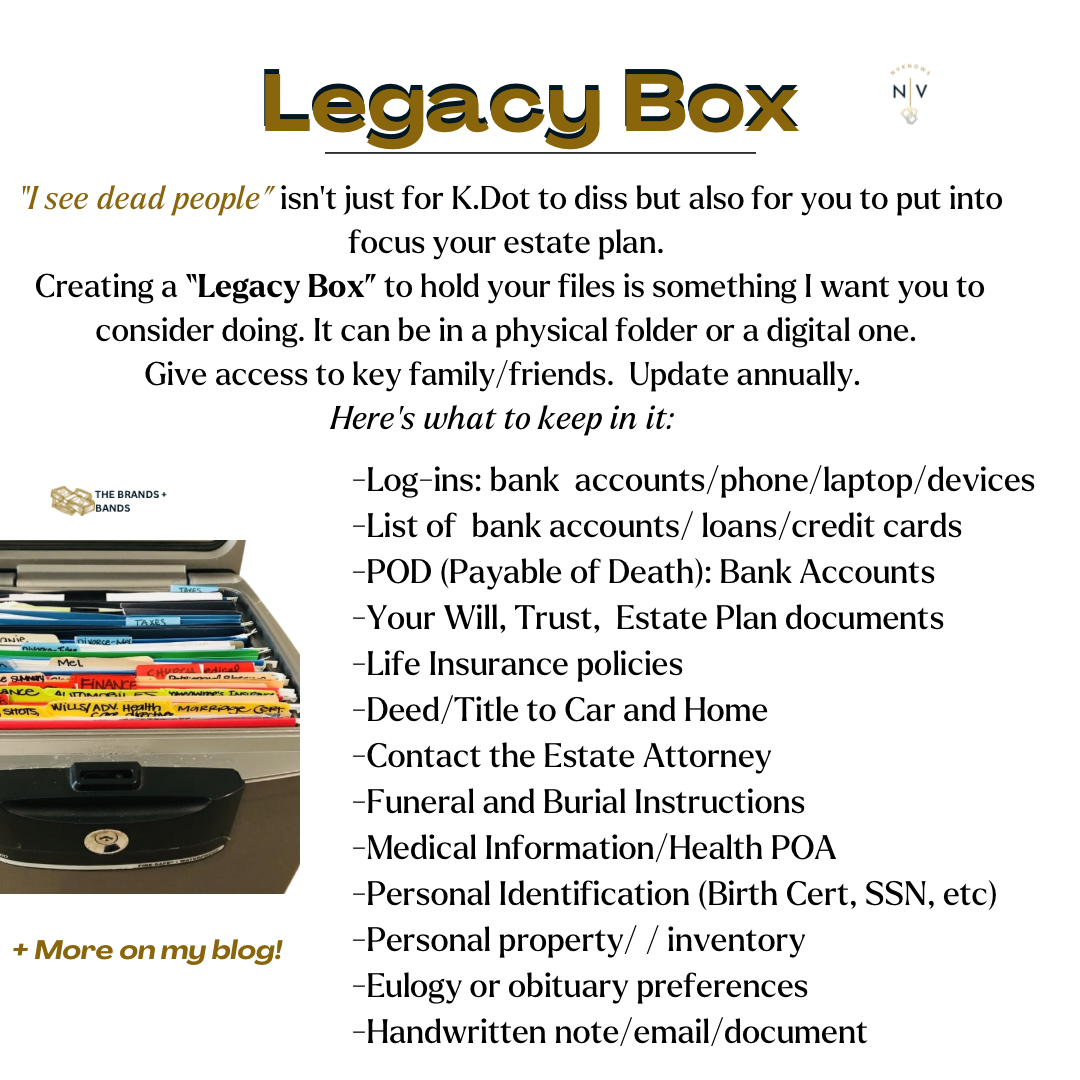

Heir Tight (virtual document vault to hold your Will, POA, and other Estate Planning documents - think a digital legacy box)

EncorEstate Plans (used them through one of my training sessions - super simple)

A tip about these platforms - make sure that after you use the document make sure that they are legally bound. Also, you update it often. I call it a Legacy Box. Here are some things you should add - digital and hard copy files (in one place).

+

I just want to start adding these types of topics in this context into the chat! Don’t let GoFundMe and Probate settle your Estate along with death to make the home going unbearable. Generational Wealth is for being able to enjoy it but also being able to make sure that your family is secure and set when you pass away.

Don’t worry if you feel that your Estate doesn’t look as massive as you want currently, we’re building as we go. Let’s talk through some tips I have, documents I suggests along with platforms I think you should research to get started with your process.

Additional content:

Importance of auditing your Estate

African Americans + Estate Planning